It’s close to the end of the year now – Asia popped their champagne, and Europe is icing its...

COMAC

As we approach the end of the calendar year, a number of airlines and leasing companies are placing orders...

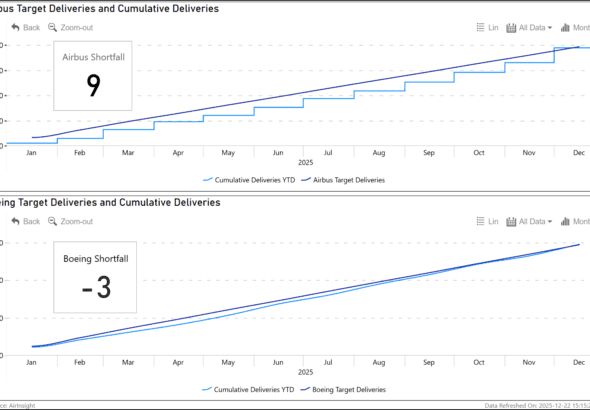

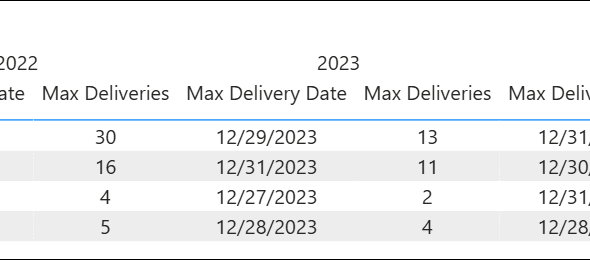

A week into the last month of the year, and here’s our score. But, first, some context. Airbus has...

It’s December, and the pressure is on. Other firms are slowing down, with annual vacations two weeks away. But...

Now that US sanctions on China have eased, we can see that COMAC is recovering. COMAC has faced US...

Another month behind us and only two months to the year’s end. 2025 is proving to be very interesting...